Final Days of Tonik Health Plans: CO, GA, NV

December 13, 2013

By Ray Wilson+

Tonik health plans, which are popular with the younger crowd due to their relatively low monthly premiums, are seeing their final enrollment dates in Colorado, Georgia, and Nevada. The final day to enroll is December 30, 2013. For all other states enrollment for Tonik is closed.

Choosing a Tonik plan will provide coverage through 2014. Some people are opting to take off-Exchange plans, like Tonik, because of the larger network of doctors and hospitals rather than choosing one of the new ACA plans: Bronze, Silver, Gold, or Platinum.

If you live in CO, GA, or NV and want a new Tonik plan call 800-930-7956 or go to HealthApplication.com.

Colorado ObamaCare Plan Extension

December 04, 2013

By Ray Wilson+

Connect for Health Colorado announced today that the Obamacare individual and family plans have been extended to December 23, 2013 for a January 1, 2014 start date. This 8 day extension gives Colorado residents more time to decide on the new Bronze, Silver, Gold, and Platinum plans.

For individuals and families looking for plans go to the ACA HealthApplication.com to find a paper application in your state. For any questions call 800-930-7956 or contact Medicoverage.

Non-ACA plans for Anthem CO, GA, NV, VA: Enroll Til Nov 15th

October 29, 2013

By Katie Banks+

Anthem is allowing residents of Colorado, Georgia, Nevada, and possibly Virginia to enroll in non-Obamacare plans until November 15th. This means that all current clients can renew their current plan for another year, as well as anyone can apply for a December 1, 2014 policy end date.

Anthem Facts for those who want to Enroll in non-ACA plans

There are few things you should know when applying for these plans:

- The premiums may be less expensive

- May have a larger network

- May have added benefits

- These plans do not necessarily cover the ACA essential health benefits

- Preexisting conditions may disqualify you (if enrolling for the first time)

If you live in one of these states and would like to learn about your options call 800-930-7956 or contact Medicoverage.

Colorado Platinum Plan Overview

August 15, 2013

By Ray Wilson+

Colorado has released preliminary Platinum plan premiums. Platinum is the top tier of all the new “metal” plans, which has the lowest out-of-pocket maximums, and your provider covers 90% of your medical costs before you hit that that max. Metal plans are defined by their percentage coverage, all much include the ObamaCare 10 essential health benefits and providers must abide by the 80/20 Affordable Care Act Rule, where providers must spend 80% of the plan total policyholders’ premiums on health care or refund their policyholders.

CO Details

Colorado Platinum plan offers a deductible range of $0 -$1,000. To see how a $0 deductible Platinum plan, we have included Covered California’s Platinum plan chart for illustrative purposes only:

| Benefits

|

Platinum Health Plan*

|

| Deductible

|

$0

|

| Preventive

|

$0

|

| Doctor’s Office Visits

|

$20

|

| Specialist

|

$40

|

| Generic Rx

|

$5 or less

|

| Brand RX

|

$15

|

| Lab Testing

|

$25

|

| X-ray

|

$40

|

| ER Visit

|

$150

|

| Urgent Care

|

$40

|

| Out-of-Pocket Max

|

$4,000/$8,000 (ind/fam)

|

Colorado Platinum Plan Premiums

For a 40 year old, non-smoker, a Platinum plan in Colorado has a range of $314 to $499. These premium rates do not include ObamaCare federal premium subsidies, which can drop the premium significantly. Remember premiums are based off age, area, and provider. For your specific premium call 800-930-7956.

Platinum Plans in Comparison to Other Metal Plans

Platinum plans are expected to enroll the sickest in society due to its low or $0 deductible, and lowest out-of-pocket maximums. If this is the case, Platinum premiums could increase drastically in the coming years. A Platinum member will pay 10% of their medical costs in comparison to a Silver Plan where the member would pay 30%. Click here to compare the ObamaCare Bronze plan, Silver plan, Gold plan, and Platinum plan side-by-side.

For further questions call the number above or contact Medicoverage.

ObamaCare Gold Plan Colorado Details

August 14, 2013

By Katie Banks+

Colorado has released its preliminary Gold plan premiums, as well as deductibles on certain plans. Nationwide all Gold plans much include the ObamaCare 10 essential health benefits, providers must cover 80% of your medical costs, and insurance companies must abide by the 80/20 Affordable Care Act Rule, where providers must spend 80% of the plan premiums on health care or refund their policyholders.

CO Gold Plan Overview

The Colorado Gold plan deductibles range from $0 -$2,000. Below is a chart of how an average California Gold Plan breaks down, purely for illustrative purposes:

| Benefits

|

Gold Health Plan*

|

| Deductible

|

$0

|

| Preventive

|

$0

|

| Doctor’s Office Visits

|

$30

|

| Specialist

|

$50

|

| Generic Rx

|

$25 or less

|

| Brand RX

|

$50

|

| Lab Testing

|

$35

|

| X-ray

|

$50

|

| ER Visit

|

$250

|

| Urgent Care

|

$60

|

| Out-of-Pocket Max

|

$6,350/$12,700 (ind/fam)

|

CO Gold Plan Premiums

The average Gold premium for a 40 year old, non-smoker range from about $287 to $551 per month. However these premiums do not include ObamaCare federal premium subsidies, which can drop the premium significantly. Remember premiums are based off age, area, and provider. For your specific premium call 800-930-7956.

The Gold Plan in Comparison to Other Metal Plans

While the Gold plan has second highest monthly premium, plans are available with “first-dollar” advantage. First dollar means that as soon as you seek care your provider pays their share. As well, as if you do get a plan with a deductible, if it follows California’s lead, Colorado Gold plans will offer many benefits before the deductible is satisfied. A plan like the Bronze plan may have a lower monthly premium, but a Gold plan, if you get sick, could save you money throughout the year. Click here to compare the ObamaCare Bronze plan, Silver plan, Gold plan, and Platinum plan side-by-side.

For further questions call the number above or contact Medicoverage.

Colorado’s ObamaCare Silver Plan Details

August 14, 2013

By Katie Banks+

Colorado has released preliminary premiums and rates for its Silver ObamaCare plans. Silver is considered the standard of the ObamaCare plans offers the second lowest monthly premium, as well as the only plan that, if qualified, have cost-sharing subsidies available. All ObamaCare plans must include the 10 essential health benefits, however each provider and state may offer the benefits differently.

CO Silver Plan Details

The Silver plan should, if it follows California’s model, provide benefits before the deductible is satisfied. Colorado’s Silver plan has a preliminary deductible range of $1,250 to $5,000. This plan has a 70/30 split, with the insurance company covering 70% of your services before you meet your out-of-pocket max. Below is a chart of California’s breakdown, just to illustrate how Colorado’s Silver plans may work.

| Benefits

|

Silver Health Plan*

|

| Deductible

|

$2,000 Med

|

| Preventive

|

$0

|

| Doctor’s Office Visits

|

$45

|

| Specialist

|

$65

|

| Generic Rx

|

$25 or less

|

| Brand RX

|

$50 *after $500 Rx deduct

|

| Lab Testing

|

$45

|

| X-ray

|

$65

|

| ER Visit

|

$250 *after deduct

|

| Urgent Care

|

$90

|

| Out-of-Pocket Max

|

$6,350/$12,700 (ind/fam)

|

CO Silver Plan Premiums

Colorado Silver premium’s range for a 40 year old, non-smoker from $245-$475 per month for an individual. These premium rates do not include ObamaCare federal premium subsidies, which can make the monthly premium drop signficantly. Remember premiums are based off age and area. For your specific premium call 800-930-7956.

Comparing Colorado Silver Plan to Other Metal Plans

While Silver has the second lowest monthly premium, it is, as stated above, the only plan that offers ObamaCare cost-sharing subsidies to individuals and families making less than 250% of the poverty line: $28,725 for an individual and $58,875 for a family of four.

So even though the Bronze plan has a lower monthly premium, Silver may save you more money because of the deductible being lower, more services before the deductible is met, and if you qualify the cost-sharing subsidies. Remember to not just weigh your monthly premium when choosing a health plan. Click here to compare the ObamaCare Bronze plan, Silver plan, Gold plan, and Platinum plan side-by-side.

For further questions call the number above or contact Medicoverage.

Colorado ObamaCare Bronze Plan Overview

August 13, 2013

By Ray Wilson+

The Health Insurance Marketplace begins enrolling October 1, 2013. The Bronze plan has the lowest monthly premium, with the highest out of pocket costs*. Colorado premiums range from the deductible offered. All plans must include theObamaCare essential health benefits.

*Some job-based plans may actually offer lower Silver plan premiums than Bronze.

CO Bronze Plans

This article deals with Bronze plans for individuals and families. Click here to learn about how the Bronze plan works for group and small businesses under ObamaCare. These plans must offer a 60/40 split with your insurance company covering 60% of your medical care. Deductibles for a CO Bronze plan range from $2,500 to $6,350. All ObamaCare plans must follow the 80/20 Affordable Care Act Rule, where 80% of plan premiums must be spent on medical care or will be refunded to members.

Colorado Bronze Premiums

For a forty year old, non-smoker Bronze monthly premiums range from $186 -$435 per month. These costs depend on area, coinsurance, deductible, and copays. These plans have a maximum out-of-pocket cost of $6,350. These premiums do not include the ObamaCare premium subsidies.

For information about your specific Bronze health plan premium call 800-930-7956.

Bronze Plan May Cost You More

The Bronze plan will cost you the least each month, but you will have to pay out pocket more with its higher deductible and fewer services covered before your plan pays.This could mean that you actually spend more per year on health care. Also, Silver is the only plan that offers ObamaCare cost-sharing subsidies to help with the costs of deductibles, coinsurance, and copays. Click here to compare Bronze Plan, Silver Plan, Gold Plan, and the Platinum Plan side-by-side.

For any questions or assistance in applying (enrollment goes from October 1, 2013 to March 31, 2014), please contact Medicoverage.

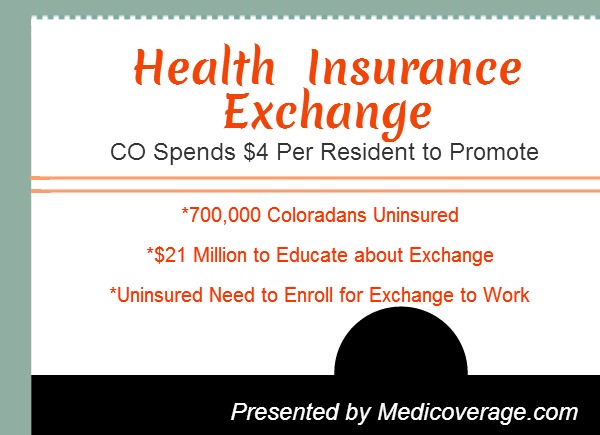

Health Insurance Exchange: CO Spends $4 Per Resident to Promote

July 24, 2013

By Ray Wilson+

Colorado spends $4 per resident to promote the new Health Insurance Exchange. This money comes from a federal grant and is being spent on advertising in both English and Spanish, as Latinos represent one of the most under served Americans when it comes to health insurance.

The total spending amount is approximately $21 Mil to help Colorado residents understand the new ObamaCare plans known as the Bronze Plan, Silver Plan, Gold Plan, and Platinum Plan. Many polls across the country are showing that most people, including doctors don’t understand how ObamaCare will affect them. This ranks them as 8th highest spender in the country to promote the new Health Insurance Exchange.

There are 700,000 uninsured persons under 65 in Colorado. Colorado is sending people to “festivals, libraries, churches and health fairs” to educate people on the reform, according to the AP. This is because the majority of the uninsured are needed to enroll in order for the Exchange to be successful.

For any questions about Colorado’s Exchange call 800-930-7956 or contact Medicoverage.

Health Care Exchange Colorado: Needs Hundreds to Sign Up Each Day

June 28, 2013

By Katie Banks+

Colorado is claiming that it needs hundreds of the currently uninsured to sign up each day for the initial ObamaCare enrollment period of October 1, 2013 to March 31, 2014. Coloradans will have an opportunity at that time to sign up for the new “metal” plans: Bronze Plan, Silver Plan, Gold Plan, and Platinum Plan.

800 Newly Insured Daily a Necessity in CO Exchange

NewsHour health correspondent Betty Ann Bowser stated, “In order to make the exchange eventually pay for itself, the outgoing insurance commissioner has said the exchange will need to sign up 800 people a day in the first six months.” That is a large number and Colorado is concerned they won’t meet that number.

The Executive Director of the Colorado Consumer Health Initiative, Dede de Percin, believes it will take some time for people to switch over. She compares this change of social consciousness to seat belts: “I was arguing with somebody about this, and they said, the fines aren’t high enough, people are never going to—and I said, seat belts. And he looked at me. And I was like, I’m 53 years old. My mother just threw her hand across my chest. And the reason why I wear my seat belt now is not because of a fine. It’s because we had that sort of cultural shift.”

Sign Up in Colorado

The good news is you don’t have to wait till the Exchange is available to sign up if you are without health insurance now. Many providers will extend coverage through December 2014, therefore it might be a good idea to lock in a lower rate now on an inexpensive plan like SmartSense CO that offers inexpensive doctor visits, a wide range of deductibles, and free preventive services.

If you are curious about plan options in Colorado or in your state call 800-930-7956 or contact Medicoverage.

Healthcare Exchange Colorado: Releases Health Premiums

June 19, 2013

By Katie Banks+

Connect for Health Colorado has released its preliminary monthly premiums for the Bronze Plan, and the Silver Plan. These plans meet all the ObamaCare essential benefits and price varies by region and provider within the region.

| Monthly Premiums

|

Bronze

|

Silver

|

| 21 Year Old

|

$146 to $234

|

$192 to $279

|

| 40 Year Old

|

$186 to $299

|

$245 to $357

|

| Details

|

Bronze Plan

|

Silver Plan

|

*The above plans are based off a person living in Denver and do not include federal premium subsidies. To learn what your actual premium will be call 800-930-7956.

Further Questions:

For any further questions contact Medicoverage.

How the Affordable Care Act Helps the Uninsured

May 31, 2013

By Amy De Vore+

The Affordable Care Act helps the uninsured in a few ways. For instance, in the LA Times today there was an article about a woman making $12.68 an hour, mother of one child, lives in Los Angeles, and recently choose to forego surgery because she was uninsured. As of January 1st this woman would have options for health coverage.

How the Affordable Care Act Helps Uninsured

She isn’t qualified for Medicaid, however since she works she may qualify for job-based insurance as 2015. Until then and if her employer doesn’t offer insurance she would qualify for premium subsidies and cost-sharing subsidies, and her daughter would qualify for Medi-Cal.

Costs for Lower-Income Families

The article doesn’t state how old she is, but if she is 30, her Silver plan premium could be as low as $93 a month and her deductible would be reduced from $2000 to $500, and a reduced maximum out of pocket from $6,350 to $2,250. This would apply to any single parent to one child living in the Los Angeles area, making her salary.

How do Lower-Income Families and Individuals Get Insurance?

First, it’s important to remember for anyone purchasing a plan from the Health Insurance Marketplace you need your W2 paperwork and financial information handy like child support, alimony, assets. Then you can either go directly through your state’s newly established call center’s navigators or you can go through your insurance agent. Many don’t realize that agents can help with on and off-Exchange plans.

Lower Income Seniors

Seniors do not have to do anything as of January 1st. Seniors stay on Medicare and do not apply for the new metal plans. Make sure your friends and parents are aware that there is nothing for them to do, because states are vocally expressing their concerns about seniors being tricked by scammers into giving away personal information due to the lack of awareness in regards to the ACA.

To learn if you qualify for a subsidy call 800-930-7956 or contact Medicoverage.

Anthem Connecticut: Exclusive Member Savings: 800-CONTACTS and Glasses.com

May 30, 2013

By Ray Wilson+

Anthem Connecticut has just teamed up with 1-800 CONTACTS and Glasses.com to offer members exclusive savings on contact lenses and eyeglasses. Anthem Connecticut members receive $20 off a $100 purchase and free shipping.

These plans are available to Anthem members of Premier CT, SmartSense CT, and Lumenos HSA CT. To learn more about the 1-800 CONTACTS and Glasses.com savings through these Anthem Connecticut plans call 800-930-7956 or contact Medicoverage.com.

Colorado Employers Offering Insurance Through ObamaCare

May 22, 2013

By Ray Wilson+

When key parts of the health care law take effect in 2014, there will be a new way to buy health insurance: the Health Insurance Marketplace, AKA Healthcare Exchange. To assist you as you evaluate options for you and your family, this notice provides some basic information about the new Marketplace and employment based health coverage offered by your employer.

What is the Health Insurance Marketplace?

The Marketplace is designed to help you find health insurance that meets your needs and fits your budget. The Marketplace offers “one-stop shopping” to find and compare private health insurance options. You may also be eligible for a new kind of tax credit that lowers your monthly premium right away. Open enrollment for health insurance coverage through the Marketplace begins in October 2013 for coverage starting as early as January 1, 2014.

Can I Save Money on my Health Insurance Premiums in the Marketplace?

You may qualify to save money and lower your monthly premium, but only if your employer does not offer coverage, or offers coverage that doesn’t meet certain standards. The savings on your premium that you’re eligible for depends on your household income. Click here to learn if your employer must offer health insurance.

Does Employer Health Coverage Affect Eligibility for Premium Savings through the Marketplace?

Yes. If you have an offer of health coverage from your employer that meets certain standards, you will not be eligible for a tax credit through the Marketplace and may wish to enroll in your employer’s health plan. However, you may be eligible for a tax credit that lowers your monthly premium, or a reduction in certain cost-sharing if your employer does not offer coverage to you at all or does not offer coverage that meets certain standards. If the cost of a plan from your employer that would cover you (and not any other members of your family) is more than 9.5% of your household income for the year, or if the coverage your employer provides does not meet the “minimum value” standard set by the Affordable Care Act, you may be eligible for a tax credit.*

Note: If you purchase a health plan through the Marketplace instead of accepting health coverage offered by your employer, then you may lose the employer contribution (if any) to the employer-offered coverage. Also, this employer contribution -as well as your employee contribution to employer-offered coverage- is often excluded from income for Federal and State income tax purposes. Your payments for coverage through the Marketplace are made on an after tax basis.

How Can I Get More Information?

For more information about your coverage offered by your employer, please call 800-930-7956 or contact Medicoverage.

* An employer-sponsored health plan meets the “minimum value standard” if the plan’s share of the total allowed benefit costs covered by the plan is no less than 60 percent of such costs.

Colorado May Not Meet the Healthcare Exchange Deadline

May 21, 2013

By Amy De Vore+

The Patient Protection and Affordable Care Act (AKA ObamaCare) kicks in fully on January 1, 2014, however, according to the state of Colorado’s official government website they may not be equipped to meet the deadline set out by the federal government, due to budgetary constraints and change of administration. Colorado is currently combining in place state legislation and future federal legislation, finding this balance is foresight driven and requires numerous hours that are quickly closing in on Colorado.

Why is Colorado saying it may not be ready?

Colorado’s main gripe with the ObamaCare deadline is the lack of funding provided for administration during the implementation of the new law, such as guaranteed issuance, implementing penalties for the uninsured, federal premium subsidies to help with monthly premiums, and ederal cost-sharing subsidies. Medicoverage is looking forward to working with Colorado to help them meet the deadline. Click here to read more about the Colorado and the Healthcare Exchange.

Why Colorado is in a prime position once they meet the deadline?

In 2009, Colorado passed it’s own Health Care Affordability Act. This act qualifies Colorado for federal matching starting in 2014, for its preemptive implementation of expanding Medicaid for those up to 100% of the federal poverty line, and 250% for pregnant women and children. Which means more money for the state.

What are other Benefits of Healthcare Exchange for Coloradans?

• 23,000 new healthcare related jobs are estimated to be established in Colorado by 2019

• $1 in healthcare spending will generate $2.44 in spending, increasing Colorado’s economy by $3.8 Bil by 2019 (projected figure)

• 18,600 young adults may stay on their parents’ health insurance plan until their 26th birthday.

• $1,510- $2,160 per year, per family, is the expected amount to be saved by Colorado families by the new law.

Further Questions

To learn more about Colorado or your state meeting the deadline call 800-930-7956 or contact Medicoverage.

ObamaCare Colorado: 4 Important Things About the Healthcare Exchange

May 09, 2013

By Ray Wilson+

The Patient Protection and Affordable Care Act for CO, better known as ObamaCare, kicks in January 2014. We have compiled a list of the most important things for a Coloradan to know.

• Every resident of the Centennial State must purchase federally approved health insurance in the open enrollment period. Those without coverage will have to pay a penalty. To read more about penalties for the uninsured please read the article Affordable Care Act: Penalties for the Uninsured.

• The federal government is offering an initial 6 month open enrollment period without penalties from October 1, 2013 to March 31, 2014. After the first year, there is only an open enrollment period for 3 months. Contact 800-930-7956 extension 0 for assistance signing up.

• Preexisting conditions are a thing of the past. In Colorado all persons are eligible for healthcare. To learn more about this read the article ObamaCare: Guaranteed Issuance for Everyone.

• Federal subsidies are available for those who earn up to 400% over the federal poverty line. To find out if you are eligible for a federal subsidy go to the article Health Care Exchange Subsidies: Do You Qualify?

For your consideration:

Colorado may not be ready to implement ObamaCare by the deadline, to learn more about this and how it affects you, read the article Colorado May Not Meet Affordable Care Act’s Deadlines

Further Questions

To learn more about Colorado and the Health Care Exchange please call 800-930-7956 the number above or contact Medicoverage: ObamaCare.

How Much Will That Operation Cost?

July 02, 2012

By Katie Banks+

One of the greatest mysteries in American health care is trying to figure out how much a medical procedure will cost even when you have health insurance. For example, if you’re pregnant and have insurance, you still will be required to pay something to have your baby delivered at a hospital, right? But how much??? No one can seem to give you a straight answer on health costs. When you bring your car to the shop you always get an estimate before they begin work. Wouldn’t it be nice if someone could give you an estimate for a medical procedure before it actually took place?

Anthem today announce a new tool to allow members estimate their upcoming medical expenses before seeking treatment. The “Estimate your Cost Tool” is available online to current members. So for example, if you purchased the Anthem ClearProtection Plan in Nevada you you could this tool to estimate your cost. They have a pretty good overview video on how it works here: Anthem’s Estimate your Cost Tool. .

If you are an Anthem member, log on to your account to get started. If you have health insurance specific questions, contact a Medicoverage agent.

Anthem Colorado to Issue Credits to members

September 16, 2010

Anthem Press Release

(Anthem) today announced that it will provide a one-time premium credit to certain of its 2010 policyholders that had individual policies of health insurance. The one-time credit will be provided to policyholders either as a premium credit on their December statement or through a check. Anthem has agreed to provide

this credit as part of an agreement with the Colorado Department of Insurance (DOI) regarding our 2010 individual rates and believes the credit is in the best interest of its members.

This credit does not apply to Colorado Major Med, Custom Plus Plan or group conversion policyholders. It also does not apply to Anthem Group Plan members who receive their insurance through an employer.

In October 2009 the Colorado Division of Insurance (DOI) approved Anthem’s 2010 individual rates for the policies that are the subject of this agreement. However, earlier this year, the DOI notified Anthem that it was initiating a market conduct examination of these rates.

Anthem is confident that its rates are appropriate, consistent with state law and in line with those of its competitors. As part of the agreement, the DOI reaffirmed our 2010 individual premiums and those rates will not change. The DOI did not levy any fine against Anthem as a result of the market conduct examination. The market conduct exam will be closed without resolution of the factual and legal issues as well as the disputes that were the subject of the market conduct exam. Anthem is not admitting any fault or wrongdoing with respect to either the factual and legal issues or the disputes that were the subject of the market conduct exam. Anthem agreed to this premium credit in order to terminate the market conduct examination so that the company can dedicate its full attention to serving its members. The total amount of credits to impacted policyholders is approximately twenty million dollars.

Anthem will notify affected members about the premium credit process in November/December 2010

Anthem to remove lifetime maximum limits on all plans

August 21, 2010

By James Wilson Jones

Anthem Blue Cross announced today that it has begun the process to remove lifetime maximum payouts to its health insurance plans. The recent health care reform legislation states that insurance plans can no longer have lifetime and annual dollar limits on “essential health benefits” as soon as September 23, 2010.

Since the U.S. Department of Health and Human Services (HHS) has yet to clarify its definition of “essential health benefits,” Anthem Blue Cross has come up with the following list of the services they believe will be affected:

- Alcoholism-related services

- Ambulance services

- Asthma education

- Bariatric surgery

- Chiropractic manipulation and osteopathic manipulation services

- Diabetic supplies

- Diagnostic services

- Durable medical equipment

- Enteral formula and food products

- Hearing aids

- Home health care

- Hospice

- Infusion therapy

- Kidney disease treatment

- Mental health/substance abuse

- Ostomy supplies

- Outpatient occupational therapy

- Outpatient physical therapy

- Outpatient speech therapy

- Pharmacy

- Physician office visit (diagnostic services)

- Preventive services

- Prosthetic devices/limbs

- Skilled nursing services

- Prosthetic devices/limbs

- Skilled nursing services

- Transplant services

- Treatment of temporomandibular joint disorder (TMJD or TMJ)

Anthem states that the listed services still may be subject to copays and other cost shares and will be phased in over time. Annual dollar limits of at least $750,000 will be allowed for plan years from September 23, 2010, to September 23, 2011. Annual dollar limits of at least $1.25 million will be allowed for plan years from September 23, 2011, to September 23, 2012.Annual dollar limits of at least $2 million will be allowed for plan years from September 23, 2012, to January 1, 2014. After January 2014 there will be no lifetime limits and annual dollar limits.

Popular Tonik Health Insurance Comes to Colorado

January 02, 2009

Medicoverage Staff

Blue Cross of California broke the mold of traditional health insurance offerings by marketing unique health plans tailored to the lifestyle and attitudes of individuals aged 19-29. Now Anthem Blue Cross Blue Shield of Colorado is targeting the same uninsured “Young Invincibles” with the same Tonik plans.

Tonik plans are simple, easy to use and affordable. Tonik covers routine doctor visits as well as the more serious medical necessities. Unlike other individual policies on the market, seeing a dentist, getting eye exams, glasses and contacts are all-inclusive within the new benefit design.

Curious “young invincibles” Colorado residents can visit and apply for tonik online or call our agent at 888 285-6334. Applicants are subject to review and approval for a plan within minutes. The plans are intentionally easy to understand and navigate. There is minimal to no paperwork and if approved, an applicant can print out a custom-designed identification card right on the spot.

To learn more, contact us or go to www.tonikplans.com